This is part 3 of a 3-part series on College + Money, and you can learn more about this topic as well as parts 1 and 2 referenced below on the Tom Talks College podcast.

How much will we really pay?

In the first part of this series, “College Costs Simplified: The 15/35/45 Rule” (episode 16) highlighted the three basic parts of college costs and an easy to remember 15/35/45 rule to give you a ballpark of the most important part: tuition and fees. Part 2 “Merit Aid: Your Teen’s Best Part-Time Job” (episode 17) went beyond sticker price to find merit aid and show you that many colleges offer generous discounts for good grades and test scores. Net Price Calculators are one more tool to understand college costs in a more personalized way.

What is a Net Price Calculator (NPC)? Where do I find it?

Net Price Calculator = financial tool found on college websites that’s designed to provide an estimate of your costs using inputs such as EFC or income and assets, family size, number of children in college, and academic data like GPA and test scores

Your Expected Family Contribution (EFC) is an index number used to determine your eligibility for federal student financial aid. This number results from the information you provide in your Free Application for Federal Student Aid (FAFSA®) form. Your EFC is calculated according to a formula established by law and considers your family’s taxed and untaxed income, assets, and benefits. Schools use the EFC to determine your federal aid eligibility and financial aid award. Your EFC is not the amount of money your family will have to pay for college, nor is it the amount of federal student aid you will receive. It is a number used by your school to calculate how much financial aid you are eligible to receive.

That last part is highlighted because some families assume that their EFC is what they’ll pay, but it’s not. It’s just one part of the financial aid process. If you’d like to calculate an estimate of your EFC, use the Federal Student Aid Estimator.

How do colleges use my EFC?

Here’s a very simplified version of the financial aid formula.

Cost of Attendance (COA) – EFC = need

Cost of Attendance is a sample budget for a first-time full-time student, and let’s use UW-Madison’s COA for in-state residents as a reference.

Tuition and fees$11,216

Room and board $13,500 (remember that these top two parts are “direct costs”)

Miscellaneous$4200 (“indirect costs” such as books, travel, etc.)

Total$28,916

So if you had an EFC of $28,916 or more, UW-Madison’s financial aid office would determine that your “need” was zero. They’re not saying you have all that in the bank or in a 529; they’re just telling you what your need is according to their formula.

If your EFC was $20,000, your need would be $8916, but that doesn’t mean you’d get an $8916 discount, scholarship or grant. You’d probably qualify for federal student loans and that would make up the bulk of your financial aid package.

This is where EFC can be misleading. It’s just one number that goes into the process, and colleges are under no legal obligation to “meet need”.

Now let’s turn our attention back to NPC’s and see some examples that range from very helpful to almost worthless.

We love you, Athens, but your NPC stinks

Colleges often use a third-party plugin for their NPC, which is why you’ll see so many that look similar. I chose the University of Georgia as an example because it’s a personal favorite even though they do not post a “merit matrix” and offer limited scholarships to out-of-state students. As soon as I saw the site, I knew the NPC would ask for very little and deliver even less. Take two minutes to work through the University of Georgia’s net price calculator, and you’ll notice they didn’t ask for any information that would lead to academic merit aid, and they asked for a range of household income instead of your EFC. This really didn’t help us get any closer to a personalized estimate other than “we probably won’t get much if anything” – and they’re using numbers from 2020-21 to boot! C’mon, Bulldogs. You can do better.

Ohio Wesleyan, you are my new best friend

After the frustration of Georgia’s NPC, I turned to one I remember as excellent: Ohio Wesleyan. After a few easy questions about my student, I entered a GPA and was immediately shown a potential merit scholarship of $28,000 per year. That’s a discount of 53%, and I’m now well below the 45 for private colleges and universities in the 15/35/45 rule.

After what I can only describe as a smiling page of their NPC that says, “Pretty cool, huh?” you’re invited to enter financial data to check for possible need-based aid.

Every NPC requires you to check a box agreeing that this is just an estimate, and even the best can never be more than an estimate – but can you see how valuable a quality NPC can be in your family’s search for accessible and affordable best-fit colleges?

MyinTuition is the (potential) game changer

It’s incredibly hard to talk about college costs, NPC’s, admissions data or almost anything college-related without veering into too many rabbit trails of exceptions and case-by-case situations. So I’ll just say a quick, “Hey, can I share one more thing before you go?” that will put smiles on some of your faces and cause others to throw up in their mouths.

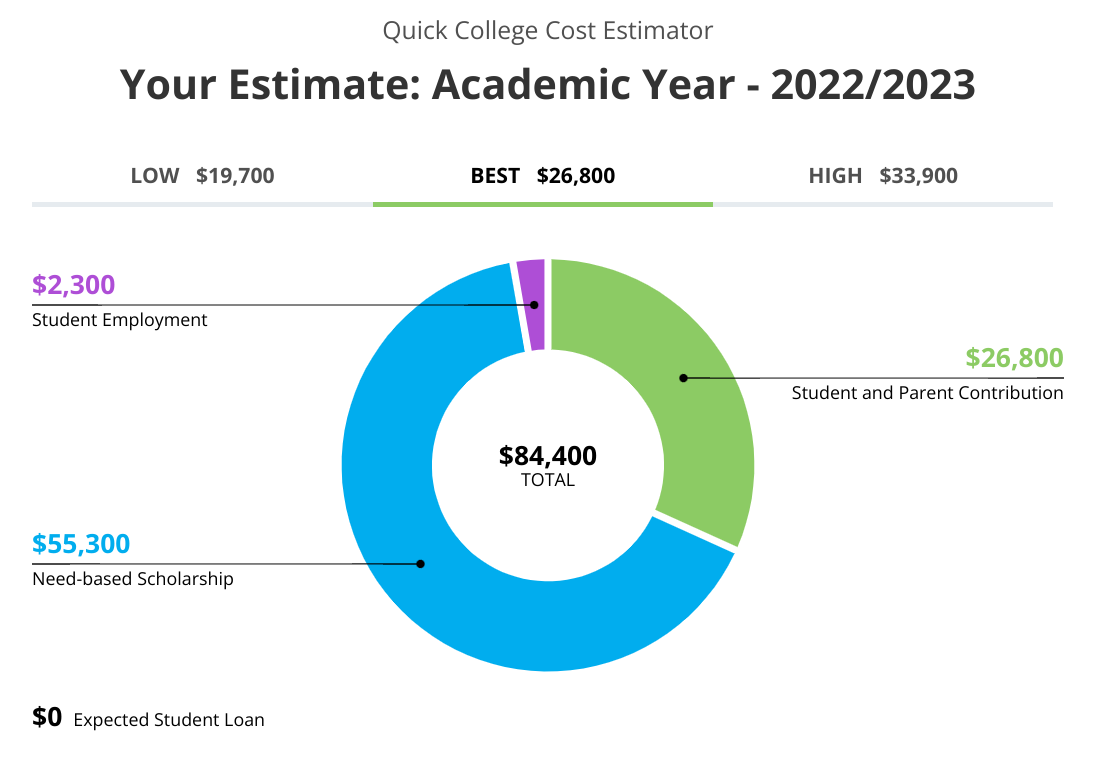

Roughly 75 of the most selective schools use an NPC called MyinTuition, sometimes in addition to a more standard version. One of the more popular “Ivy Plus” colleges is Vanderbilt, where the COA is just north of $84,000. Gulp. MyinTuition prides itself on ease-of-use and minimal questions, so let’s pretend we have one more boy in the house who is a junior and really loves him some Nashville. I’m plugging in our numbers now and will time myself and record my response as accurately as possible. (I’ve done this for others on the list but not the Commodores.)

It took just under two minutes, and I shook my head with a pleased “hmmm” when I saw these numbers.

The Kleese’s are kicking in $26,800, unnamed son #3 will work at the library or set up chemistry labs as his dear mother did to earn $2300 – and Vanderbilt picks up the tab for rest. MyinTuition always gives you a best estimate as well as a low and high, and when I click on those I just see our green part moving with the blue part adjusting as well.

This is great, right? Our EFC this year was around $40,000, so if you jump back to UW-Madison, we’re likely only qualifying for student loans but no scholarships or grants. And Vanderbilt is less than the $28,916 full price tag at Madison.

Now all we need is to adopt a super smart kid who can get into Vanderbilt, and then I’m the dad in the dad-polo enjoying an SEC game.

Your results may vary

Some of you are in different financial situations than we are, and I’ve sent MyinTuition out to enough parents and had enough “are you crazy?” responses to know that the green piece of their puzzle is sometimes overwhelming. But that’s still a good thing – because knowing or even expecting to pay whatever your costs may be is so much better than telling your student to “not worry about price and if you get it we’ll figure it out”. Will you? Should you even say that unless you have some basic information like this?

What now? Run some numbers!

Schedule one hour this weekend in a quiet room to calculate your EFC, and then use that number in NPC’s at colleges that interest you or your student. Seriously – one hour will teach you so much you didn’t know, and even if you don’t like what the NPC’s show you…at least you’ll know.

Call me at (608) 553-3445 and say, “Hey, I read the blog and listened to the podcast and did that one hour thing you suggested, and I just wanted to talk a little more about this.” I’d love to take that call and help you understand not just what I said and showed you, but listen to what you’re seeing and thinking, and then answer as many questions as I can on a phone call.

Here’s how I got the 1.3% number, because it’s not percentage-based.

UW-Madison COA of $28,916 x four years = $115,664

Our standard college search package is $1500. $1500/$115,664 = .0129685987, or 1.3%

Up next

Here’s an email from a parent: “Excellent merit aid podcast…I think you should do a podcast directed to the students about how to not stress out about this entire process. Maybe one for type A moms.”

This is part 2 of a 3-part series on College + Money, and you can learn more about this topic and also hear last week’s “College Costs Simplified” on the Tom Talks College podcast.

Merit aid may be the best thing you’ve never heard of when it comes to college admissions, and what follows is a quick introduction to what could be your teen’s best part-time job…and to the gift that keeps giving. Before we dig into the details, let me state this up front and as clearly as I can.

Merit aid is the best tool you have to reduce the cost of college.

Read that again, and if it helps, imagine me as Curly from “City Slickers” holding up one finger to you, the Billy Crystal character, but not dodging your question about what the one thing is – because it’s merit aid. Plain and simple.

What exactly is merit aid?

Merit aid is a general term for scholarships you earn that come directly from colleges. You’ll sometimes see these listed as freshman scholarships, and they are awarded for talents such as athletics, fine arts, or academic achievement. Just as important is what they are NOT. Merit scholarships are NOT:

Loans;

Need-based financial aid;

Distributed by the federal government.

The bulk of merit aid is “automatic”, in that it’s awarded by hitting key benchmarks in cumulative GPA and ACT/SAT scores. (By comparison, “competitive” scholarships are those to which you apply after acceptance and are usually awarded to only a handful of students. If you see a long list of scholarships with the donors’ names attached, those are competitive.)

For academic merit aid, admissions offices pull GPA and ACT/SAT numbers, if applicable, straight from your student’s application, and many colleges openly display what I call a “merit matrix” – a simple chart with rows and columns for grades, test scores and money. The first example I saw was on Miami University’s website, and I almost fell off my chair.

The gift that keeps giving

Unlike scholarships that are handed out at high school awards nights, merit aid is awarded all four years assuming the student maintains satisfactory grades.

You, the hard-working, bright high school student, spend three years building up that nice GPA and knocking out some impressive standardized test scores – and you’ll be handsomely rewarded throughout four years of college.

Where and how to find it

In general, you’ll find merit aid in two types of colleges:

Public universities in states hoping to attract bright young minds and boost not only the academic stats of an incoming class, but their ranking in US News and World Report.

Private colleges and universities that aren’t members of the Ivy League or among the most highly selective.

The first category is a little easier to find and often comes with a merit matrix. The second category is less evident and less likely to be upfront about automatic merit aid, but it’s still a prime source of merit aid.

There is no central database or comprehensive list of colleges that award merit aid, so your best bet is to Google [name of college] and then a combination of these terms: merit aid, merit scholarships, freshman scholarships.

I often plug out-of-state into my search, because I’m usually searching for options beyond a student’s home state. Be sure to compare in-state vs. out-of-state merit when you find it, because those numbers can vary greatly.

Notice there are two levers: cumulative GPA and ACT/SAT. Alabama uses two GPA ranges (3.50+, 3.00-3.49) which is fairly common. Sometimes you’ll see one level stacked on top of the next, i.e. 3.50 + 26 ACT, 3.75 + 28 ACT, 4.00 + 30 ACT. And in full transparency from a business which was built on test prep, some colleges shifted to a GPA-only approach in 2020 so you really do need to look at each college individually.

Why are they doing this? Is there a catch?

Way before NIL, colleges aggressively recruited 5-star athletes to boost on-field success – and some have taken a similar approach to academics. A seminal article on the merit aid movement was published in the New York Times on November 3rd, 2016: How the University of Alabama Became a National Player.

Rule of thumb for merit aid

The harder it is to get into a college, the less likely you are to get merit aid. Their gift to you is the fat envelope. The Ivy League doesn’t award merit because they don’t have to, and neither do the hyper-popular-and-competitive public flagships like UNC-Chapel Hill. In fairness, they do offer some but I’ll let you read this and then decide what your chances are.

UNC is proud to offer Academic Scholarships to a small number of outstanding students each year. All students who are admitted to UNC are automatically considered for these scholarships; no additional application materials are necessary.

Unfortunately you’ll quickly run into colleges which don’t offer merit aid, or are much less transparent, using language to the effect of “we provide scholarships for deserving students in recognition of their achievements.” “ (On a future podcast and blog I’ll coach you on how to use Net Price Calculators as a possible work-around.)

Great values beyond flagships

Medium-sized private universities that accept over half of applicants are a great source of merit aid. Marquette, for example, almost always knocks off a quick $16,000-$20,000 in the acceptance letter. Regional comprehensive universities similar to UW-La Crosse or Winona State also offer tremendous value. The snowboarder or mountain bike enthusiast who ventures to Colorado Mesa University in Grand Junction packing a 3.75 and a 29 ACT will be rewarded with $6000/year, and that’s coming off an already low out-of-state tuition and fees cost of $15,000 after CMU shows you some love with their tuition discount programs.

Seriously…if your kid digs the Colorado thing, especially that corner over by Utah, New Mexico and Arizona…why wouldn’t you take a hard look at Colorado Mesa?

Your teen’s best part-time job

I wrote that phrase – your teen’s best part-time job – not to suggest that 16-year-olds shouldn’t bag groceries or mow lawns or be a nanny. I just want to be painfully clear that efforts and achievements in the classroom can have tremendous potential ROI, and should be taken as seriously as the time spent working, playing sports or practicing the oboe.

It’s not my goal to put pressure on your kid to be a 4.0 student. I just want them to understand that grades and test scores don’t just happen, and sometimes a small amount of effort or just attention to detail makes a big difference. The billboard I’d put up has a simple message that all students can achieve.

Turn in all your homework. On time. All the time.

I’ll skip the $8000 German take-home vocabulary quiz story mentioned on the podcast.

Merit aid is real and it’s within your reach

For the vast majority of students, a merit scholarship based on academics is far more likely than an athletic, music or theater scholarship, and probably reduces your costs of higher education significantly more. So know what matters to colleges in terms of admissions but also in terms of merit aid, and let your student know early on. We did this with both our sons when they were in middle school, and both earned merit scholarships for out-of-state public universities that saved them and us tens of thousands of dollars.

Having a conversation beyond the numbers

If you’re struggling with any part of this – or if you just want to talk to someone who thinks about this everyday – email me anytime or schedule a free consult and let’s talk not just about the numbers, but about your family and your students, and what you hope to achieve.

Comparing costs at different colleges is often more complex than it needs to be, partly due to a lack of consistency from one college website to another. If you’re not careful, you run the risk of making decisions based on faulty information.

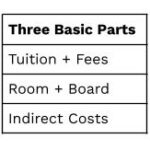

In this blog and in episode 16 of Tom Talks College, I’m going to break down costs for any college into three basic parts that are universal and can easily be compared. You’ll also learn a rule of thumb for typical costs at different types of colleges – including out-of-state and private – and you’ll learn how to use simplified numbers to make easy but more accurate comparisons between colleges.

This is the first in a series of three lessons on college + money. Next week you’ll learn about merit aid – the gift that keeps giving, and your teen’s most profitable part-time job – and the following week you’ll learn how to calculate your Expected Family Contribution, and how to use that EFC number to better estimate your costs at different colleges.

Know the 3 basic parts and be sure to “bundle” T & F

Too many times I’ve heard people compare one college’s tuition to another college’s Cost of Attendance, a comprehensive budget that includes much more than just tuition. That’s like comparing the principal you’ll pay on a new house to the PITI (principal interest taxes insurance) on another. It’s bad math and it prevents you from making wise decisions.

So the first step is to understand the three basic parts of the cost of college. Think about the three parts as learning (tuition & fees), living (room & board) and lattes (indirect costs – more on that later). Tuition and fees is where we’ll spend the most time – because that’s where you’ll spend the most money – and because it varies way more from college to college than the other two. And always look for the combination of the two, because some colleges post tuition and are less forthright about fees. (There’s a trend in higher education to shift more expenses to fees in an effort to keep tuition flat.)

Let’s focus on tuition & fees and look at national averages for four-year colleges and universities for 2022-23. This data is from the College Board’s Trends in College Pricing report, and I’m rounding these off as a first step towards simplification.

In-state public universities = $11,000

Out-of-state public universities = $28,000

Private colleges and universities = $39,000

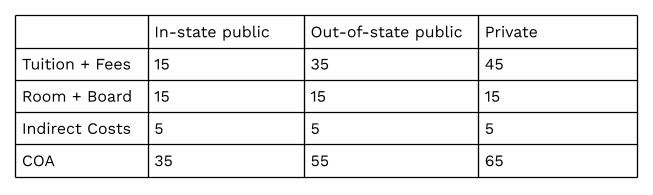

The 15/35/45 rule

What’s more valuable than averages, however, are the numbers you’ll likely see in each of these categories for the schools that most interest you. Let’s call these typical costs, and here’s an example of why it will be more helpful to use a higher number than the averages.

The out-of-state public university average of $28,000 includes Colorado State-Pueblo, Colorado Mesa and Adams State, all fine schools and all located in the great state of Colorado. Their tuition and fees are included in the averages, and all fall well below $28,000, which is great. What’s no so great, however, is that if you don’t live in Colorado, you’re much more likely to be interested in CU-Boulder where the tuition & fees are $40,396 to $43,960 depending on your major, or Colorado State which is $32,734. So the typical cost we’re going to use for out-of-state public universities is based on “flagship” schools, i.e. the one or two biggest and most familiar names in each state.

The same is true for private colleges and universities. A quick analysis of six popular Midwestern private universities (St. Thomas, Marquette, Drake, Butler, Xavier and Creighton) reveals average tuition and fees of $47,860.

I’d rather overestimate costs of anything and be pleasantly surprised when something comes in lower, so here’s how we’ll adjust averages to more useful typical costs.

Notice that we’ve knocked off three zeros to arrive at the 15/35/45 rule.

Apples to apples

Let’s look back at CU-Boulder and CSU now that we have the 15/35/45 rule and see how each compares. Buffaloes in Boulder will pay 40 to 44, which is 5-9 above, and CSU Rams will pay 33, which is a modest but welcome 2 less. Obviously that’s just one data point and now we need to look at room & board, indirect costs, and financial aid to get a more complete picture. But do you see how knowing the 15/35/45 rule quickly puts everything into context?

We’ve only talked about tuition & fees because that’s the biggest chunk of the three basic parts, and it’s the most variable, but your student needs a place to sleep and eat, too. The national average for room and board is $13,000 and that’s what I’ve used as an easy number for several years, but I’m afraid it’s time to adjust that to $15,000. Room & board costs are rising more quickly than tuition & fees, and you’re less likely to spit out coffee if you plan for 15 and the real number comes in lower.

A quick word about lattes and indirect costs…

All colleges create an estimated annual budget for a first-time full-time student living on campus and taking a full load of classes. It’s called “Cost of Attendance” and must include the things you pay directly to the college (tuition and fees, room and board) and also the common expenses such as books and supplies, travel and miscellaneous expenses (sometimes referred to as personal expenses). Here are national averages:

Books & supplies = $1200

Travel = $1200

Miscellaneous = $2220

That’s $4600 total but colleges really vary on their estimates, plus something like travel could be widely different based on location. Use a simple 5 for typical costs.

To be honest, I don’t even pay attention to indirect costs. I only focus on the two parts that make up direct costs. Is that poor financial planning? No, because I’m pretty sure that what you spent on club volleyball, prom, and feeding a teen adds up to more than $5000 per year. So think of it as a wash.

Let’s pause for a second to remind ourselves that all of these numbers are subject to change based on financial aid, so we’ve only been looking at sticker prices up until this point. Next week I break down what merit aid is and why an understanding of it is critical to opening up options outside your state and beyond public universities. Merit scholarships open doors you didn’t know existed.

Now let’s put all three parts together to see typical Cost of Attendance figures for all three types.

These are big numbers. Scary numbers, perhaps. That’s why you need to tune in next week because the middle and the right columns have something you need: merit aid.

If you’d like to hear a few more examples of how actual costs compare to typical costs, and how you can quickly go from not knowing the costs of a college to wrapping your head around it and being able to see if it’s a possible financial fit, listen to the second half of episode 16 of Tom Talks College. In addition to this college + money series, you’ll find practical guidance on everything from campus visits to finding the right college to standardized testing to suggested timelines for your student.

Having a conversation beyond the numbers

If you’re struggling with any part of this – or if you just want to talk to someone who thinks about this everyday – email me anytime or schedule a free consult and let’s talk not just about the numbers, but about your family and your students, and what you hope to achieve.

Paying for college and who pays for what and when is among the most challenging topics between teens and parents. In your family, does everyone understand who pays for what and when for college costs? For most families, the answer is no.

Most families aren’t talking early enough or often enough about who pays for college. Not enough families are openly asking enough questions of each other when it comes to who’s paying for what college costs and when. In its most recent survey of college costs, the College Board reports that the average cost of attendance for in-state students at a four-year public institution for the 2020-2021 academic year averaged $26,820. This means that even an in-state, public college education is a six-figure decision. It warrants clear conversation about who’s paying for college costs or how college costs will be shared among parents and the student.

Do yourself a favor when it comes to determining who’s paying for college.

On or before your child’s 12th birthday, please have this conversation: “We think it’s important for you to go to college, or at least consider your college options. Here’s what we’re going to do to help…” If your student is older than 12, then have the conversation as soon as possible once you and your spouse or significant other come to agreement about who pays for college and your family’s college cost arrangement.

Families that fail to address the college cost question suffer from consequences of poor communication and poor planning. Even if it’s uncomfortable, speak openly and in quantifiable terms about all three components of this college planning question: who, what and when. Who pays for college? What college costs are covered by parents, and what college costs are covered by the student? When (and under what conditions) will college costs be covered? None of these variables is optional when it comes to paying for college.

Why it’s tough to talk about paying for college.

When you shop for a car, new or used, you can assume that the price you see on the window sticker or scribbled across the windshield is not the final price you will pay. Factoring in a trade, the actual price may be 5, 10 or even 20% lower than that of the sticker. We all have a ballpark price in mind when we visit an auto dealer, or we can access one in a blue book. Houses are largely the same, but without the possible trade-in value. The people who determine college costs, however, seem to go to great lengths to prevent you from feeling any sort of comfort level or command of what you’ll pay for college. College tuition may be $25,000/year, but you really have no idea what you will pay with everything thrown in. In fairness, great strides have been made by institutions of higher learning (with considerable arm twisting from the federal government) to get you a ballpark figure early on in the college planning process using tools such as net price calculators.

Outline who’s paying for college and which college costs are covered by whom in writing.

How do you talk about who will pay for what for college (and when) if you don’t know how much college will cost? Starting college research early helps you develop solid cost estimates to work with. College websites are now much more helpful in helping you to get a sense of what you’ll pay for college.

Once you’ve done your college research, write it down, and do the math. Make it clear to both parents and to the student who’s paying for which colleges costs and what the totals are per year. Create a college cost template based on what you as a parent can and are willing to contribute. This template spells out the college financing categories (or portions thereof) for which each party will be responsible. Here are four examples:

“Mom and I will pay for all tuition, fees and books at an in-state public university. Everything beyond that is yours.”

“We will contribute $30,000 per year for four years. If you go somewhere more expensive or take more than four years, you’re responsible for the balance. And no, we will not ‘refund the difference’ if you graduate in three and a half years or choose a very inexpensive option.”

“It’s 50-50 all the way.”

“We’ll pay for everything, but we want you to work at least ten hours per week so you learn how to manage your time, just like in the real world. You can keep what you earn, but you have to work.”

As one college planning example, my parents paid for tuition and fees plus a book allowance and required each of their three sons to pick up the tab for room and board, plus spending money. Each of us chose public universities, but the idea was that we would have the option to attend a more expensive private institution without incurring significantly greater debt. For the most part, room and board is the same at Harvard as it is at Des Moines Area Community College.

You’re essentially creating a college financing contract, and it’s perfectly acceptable to include performance clauses. Setting basic benchmarks such as “satisfactory progress in all courses” or “maintain a 3.0 cumulative GPA” works well. Whether or not you put this onto paper is up to you, but the basic premise of “If I do this, I expect you to do that” helps eliminate surprises.

Bring to the college planning conversation your own experiences and arrangements with your parents, but keep in mind that working your way through college has become significantly more difficult as college costs have escalated. In fact, this approach can actually be counterproductive if a student devotes so much time and energy to earning money that she is left with little time to study. She ends up working extremely hard to pay for something that has less than optimum value.

Many families simply tell children not to worry about college costs, or not to worry about it while searching, but this can cause confusion. Instead, have the college cost conversation wrapped up prior to senior year. If the message is, “Don’t worry about it for now,” the impression you leave may be that money is no object or that a student really shouldn’t worry and therefore not plan and save for her college financing portion.

College planning questions to consider when it comes to paying for college.

How does an intended major impact this question, i.e. am I as a parent more willing to support a future anesthesiologist vs. an anthropologist?

If a student delays admission by taking a “gap year”, how does that change things?

Who gets credit for merit scholarships?

How about study abroad programs? Who pays for that?

What stipulations are there for semesters beyond the traditional four years?

How does a possible journey into grad school factor into all of this?

Making the effort to have open, honest conversations about money and college financing is far better than the consequences of NOT having these conversations. Be bold. Be open. You’ll be glad that you were.

We’ve helped thousands of students and families over more than 10 years, and can lend insight to your college cost and college planning conversations. Email me anytime or schedule a free consult to get your college questions answered.

Talking about college and money has probably edged out sex and drugs on the list of conversations parents LEAST want to have with their teenager. Maybe it’s because there’s no marketing campaign to go with it. So consider this a start toward that end. Parents, have the conversation with your kids about college and money!

Avoiding college planning pitfalls means being willing to have the challenging conversation about college and money, who pays for what and when.

Why do families avoid having the college money conversation? Lots of reasons based on my experience with hundreds upon hundreds of college-bound families.

First off, no one really knows what it will cost. We’ve all heard scary news stories about skyrocketing college costs, but we avoid getting to the bottom of what we’re really talking about here. Is it a hundred grand, or a quarter of a million dollars? How much will merit aid lower the cost? What financial aid might we be eligible for? Families are afraid to have the money talk because they feel completely inept and unprepared.

The people who determine college pricing go to great lengths to prevent you from feeling any sort of comfort about, or command of, the final price. Tuition may be $25,000/year, but you really have no idea what you will pay with everything thrown in. In fairness, great strides have been made by institutions of higher learning (with considerable arm twisting from the federal government) to get you a ballpark figure earlier in the process, using tools such as net price calculators.

In its Trends in College Pricing 2014, the College Board reported that the average estimated budget (often called Cost of Attendance) for an in-state public university is $23,410 for the 2014-15 academic year. For a private non-profit four-year college that number is $46,272.

I have heard the following phrases more than once from intelligent, well-meaning, loving parents to their children:

Don’t worry about college costs.

We’ll help you however we can.

We’ll talk about this later, when the time is right.

A friend once told me she didn’t think it was any of her children’s business what she and her husband were doing to prepare for college expenses, because their financials matters are private. I agree that my kids don’t need to know what we have saved for retirement or how much we earn, but I do believe it is in the best interests of all involved to be transparent about expectations and responsibilities.

One of the most common conversations I have with the families I work with revolves around college costs. So many factors go into what college will cost, not the least of which is which school you choose. We start by breaking down misperceptions, such as “public institutions will always be cheaper than private” (not true), and “we’ll never get any aid, so I’m not even going to fill out the FAFSA”. (Big mistake!) Step by step, we eat the elephant a bite at a time, and examine it for what it really is: a super huge investment that will pay big dividends, if it’s done right.

When it comes to college and money, who pays for what and when?

On or before your child’s 12th birthday, please have this conversation:

“We think it’s important for you to go to college, or at least consider the options you have. So here’s what we’re going to do to help…”

If your child’s older than 12, don’t panic. But have the conversation. SOON.

The answer to this question is incredibly personal. THERE ARE NO WRONG ANSWERS. Don’t avoid having the conversation because of what you assume “most families are doing” or because of your discomfort with what you’re able to do (or unable to do) as a parent to contribute to college costs.

When our oldest son was a toddler, my dear wife and I had a series of conversations about our respective philosophies about paying for our sons’ college education. We had two different philosophies within the same household! My wife insisted we pay for the entire cost of college, including room and board and incidental expenses, because this is what her parents had lovingly and generously done for her.

Then we faced facts about how college costs have changed in the past two decades. And we openly acknowledged that we started having children later in life than her parents, putting us that much closer to retirement, another expensive investment to prepare for.

I then shared my personal feelings that our two sons should have some skin in the game.

Through a lot of dialogue between us, some of it pretty tense, other conversations merely intense, we arrived at a unified position that we could then share with conviction and in detail with our two sons, in plenty of time for them to make their own preparations to put up their share of the costs, or at least make a dent in the first couple of years.

If you ask my boys how much they need to save for college, my older son, who’ll be a college freshman this fall, knows the number to the five-spot. And my younger son, a freshman in high school, at least has a solid idea. He knows what his responsibilities will be, what we’re covering, and a pretty good dollar-amount estimate for each chunk.

Families that fail to address the question of “Who pays for what and when?” risk the collateral damage that is caused by poor communication and the poor planning it leaves in its wake.

Talk openly about college and money and who pays for what and when.

Who. What. When. None of these variables is optional.

Some options could look like this:

“Mom and I will pay for all tuition, fees and books at an in-state public university. Everything beyond that is yours.”

“We will contribute $30,000 per year for four years. If you go somewhere more expensive or take more than four years, you’re responsible for the balance. And no, we will not ‘refund the difference’ if you graduate in three and a half years or choose a very inexpensive option.”

“It’s 50-50 all the way.”

“We’ll pay for everything, but we want you to work at least ten hours per week during college, so you learn how to manage your time, just like in the real world. You can keep what you earn, but you have to work.”

What you’re doing is creating a contract. And it’s acceptable to include a performance clause such as maintaining a 3.0 and making progress towards a degree. Whether or not you put this onto paper is up to you, but the basic premise of “If I do this, I expect you to do that” will go a long way toward eliminating surprises.

Okay, now it’s college money conversation homework time.

A Free Guide to Avoid pitfalls like NOT having the college money conversation, plus 5 other Critical Questions and answers.

In your situation, who pays for what & when? Be prepared for open (and at times uncomfortable) dialogue about your desired “contract” and especially the values you hope it conveys to both student and parents (i.e., sharing in the sacrifice, providing the student with ample options, making sure your family can also cover the cost of other family priorities, etc.)

If you’d like help with the college money conversation, or other college topics like ACT test prep, college applications guidance, merit aid, finding the right college and more, Schedule A Free Consult. Let’s get the college conversation started.

On or before your child’s 12th birthday, please have this conversation: “We think it’s important for you to go to college, or at least consider your college options. Here’s what we’re going to do to help…” If your student is older than 12, then have the conversation as soon as possible once you and your spouse or significant other come to agreement about who pays for college and your family’s college cost arrangement.

On or before your child’s 12th birthday, please have this conversation: “We think it’s important for you to go to college, or at least consider your college options. Here’s what we’re going to do to help…” If your student is older than 12, then have the conversation as soon as possible once you and your spouse or significant other come to agreement about who pays for college and your family’s college cost arrangement. How does an intended major impact this question, i.e. am I as a parent more willing to support a future anesthesiologist vs. an anthropologist?

How does an intended major impact this question, i.e. am I as a parent more willing to support a future anesthesiologist vs. an anthropologist?

On or before your child’s 12th birthday, please have this conversation:

On or before your child’s 12th birthday, please have this conversation:

Recent Comments